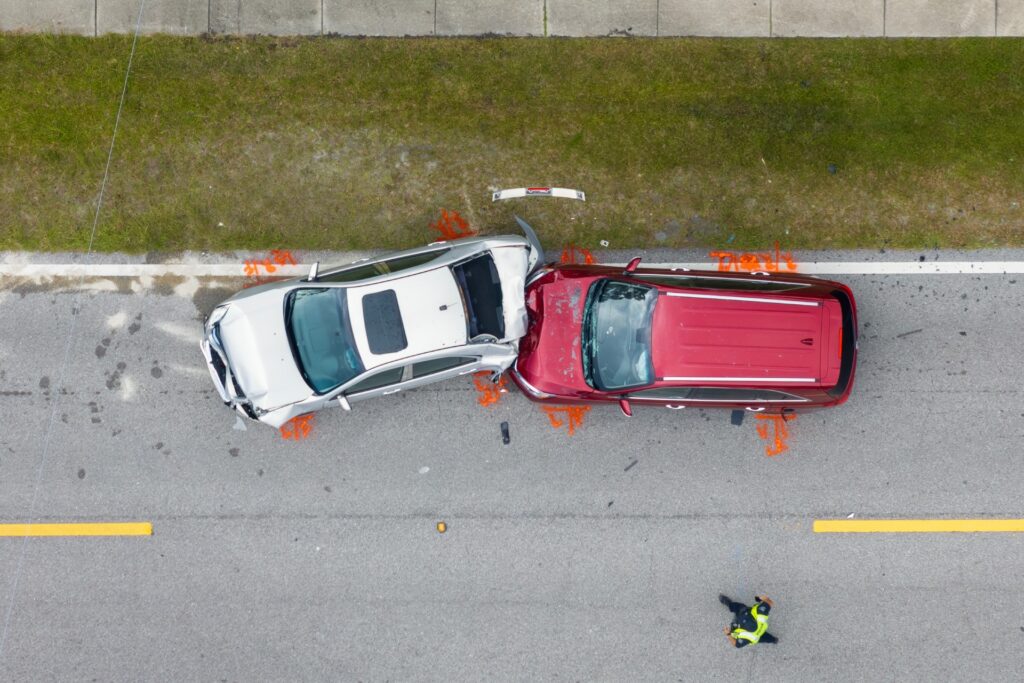

You're driving through Miami traffic when a light changes fast. A brief hesitation. A misjudged turn. The impact is immediate. In the moments that follow, the questions start. Who decides fault? What does insurance cover? What happens when you may be financially responsible for a motor vehicle accident? Learn more from our Miami car accident attorneys.

On Florida roads, a traffic accident occurs about every 44 seconds, according to the Florida Department of Highway Safety and Motor Vehicles. That level of frequency explains why fault determinations and insurance disputes are part of everyday driving risks across the state. You can also review our case results.

Being at fault shapes what happens next. An insurance claim may follow a different path. Financial responsibilities become immediate. Legal exposure may arise even when vehicle damage or injuries appear limited at first. Many drivers leave the accident scene unsure how fault is determined or which decisions matter most.

Here's what's coming: Visit our client reviews page to learn more about JDLE Lawyers.

- How insurance companies determine fault after a traffic accident

- What liability insurance means for coverage and financial responsibility

- What to do after a car accident that is your fault

- When speaking with a car accident attorney in Miami, Florida makes sense

How Is Fault Determined in a Car Accident?

Fault in a car accident is not decided by the drivers involved. It is not settled by roadside conversations or early impressions. After an auto accident, fault is determined through a review process that unfolds over time and relies on documented accident details.

Two primary decision-makers shape how fault is assigned:

- Law enforcement, which prepares a police report, documents the accident scene, notes traffic laws, and records witness statements

- Insurance companies, which investigate how the accident occurred and how insurance coverage applies

Insurance companies determine fault by reviewing vehicle damage, written or recorded statements, traffic laws, and photographs. Early assumptions can change as information is compared.

That is why fault in a car accident is often determined after review, especially when more than one driver may share responsibility.

Comparative and Contributory Fault Explained

Fault in a car accident is not always an all-or-nothing determination. In many cases, responsibility is divided based on each driver's actions leading up to the crash. Florida uses a comparative fault system, which means more than one party may be held legally responsible for an accident.

Understanding how fault is shared is important because even partial responsibility can affect insurance coverage, claim value, and financial exposure after a collision.

How Fault Is Shared Between Drivers

Fault is not always assigned to one driver. In many crashes, investigators find that responsibility is shared. Small decisions made before impact often matter. Speed, following distance, and vehicle positioning all factor into how fault is evaluated.

Because crashes unfold quickly, fault analysis looks at context rather than a single mistake. Even a driver who did not cause the collision outright may still carry partial responsibility. That shared responsibility becomes important once claims and liability are reviewed.

Why Fault Percentages Affect Financial Outcomes

Fault is typically expressed as a percentage assigned to each driver. One party may carry most of the responsibility, while another holds a smaller share. Those percentages directly influence how an insurance company evaluates payment and exposure.

Partial fault can reduce how much compensation is available. It can also shift responsibility for medical bills, vehicle repairs, or lost income. Even limited fault may leave a driver responsible for a portion of the other party's losses, which is why understanding fault allocation early matters.

What Happens If You Are Liable for an Accident?

Liability means responsibility. When you are liable after a car accident, claims may be opened against your car insurance policy for property damage and medical expenses. Lost wages may also be claimed. That responsibility exists even if injuries were not obvious at the accident scene.

Liability can affect:

- Vehicle repairs and repair costs

- Medical bills and hospital bills

- Lost wages and future medical costs

- Ongoing disputes over insurance coverage

When damages exceed policy limits or fault is disputed, legal fees and further claims may follow. This is often when drivers realize what happens if you are liable for an accident can extend beyond initial repairs.

What to Do After a Car Accident That Is Your Fault

After a collision, it is easy to feel pressure to explain what happened or accept blame. Confusion and concern about damage or injuries can push drivers to act quickly. Even when fault seems clear, knowing what to do after a car accident that is your fault helps to protect the insurance claim and avoid early mistakes.

- Stay at the accident scene and check for serious injuries

- Contact law enforcement to create a police report

- Exchange insurance information without giving a written or recorded statement

- Photograph vehicle damage, vehicles involved, and road conditions

- Notify your car insurance company promptly

These steps do not determine fault on their own. They help preserve accident details and keep the record clear while an insurance adjuster reviews what happened. Acting early helps reduce confusion and avoid disputes as the claim progresses.

Mistakes to Avoid After an At-Fault Accident

After an at-fault accident, small missteps can create larger problems as insurance claims move forward. Decisions made in the hours or days following a crash often affect how fault is evaluated and how liability is assigned.

Avoiding common mistakes helps protect the accuracy of the claim and prevents unnecessary complications during the insurance review process.

Admitting Fault Too Early

Mistakes often happen in the first moments after a crash, when stress and confusion take over. Drivers may feel pressure to explain what happened or to apologize at the scene. Even casual statements can be interpreted as admissions once reports and statements are reviewed.

Fault determination happens later, based on evidence and investigation. Accepting responsibility too quickly can complicate that process. What feels like a simple explanation in the moment may create problems once insurers begin evaluating liability.

Failing to Document the Accident Properly

Documentation errors can also create lasting issues. Leaving the scene without a police report, skipping photos, or overlooking details limits how clearly the accident can be evaluated later. Missing information often leads to conflicting accounts.

Providing a written or recorded statement too soon can add risk as well. Early statements made under stress may be incomplete or inaccurate. Those gaps tend to surface during the insurance claim process, where clarity matters most.

Delaying Medical Evaluation

Medical decisions after a crash carry long-term consequences. Some drivers delay care because symptoms seem minor or manageable at first. Others wait simply to avoid inconvenience.

Delays can weaken injury-related claims. When treatment begins days later, insurers may question whether injuries are connected to the accident. Early medical evaluation helps protect both health outcomes and claim credibility.

How Car Insurance Works in an At-Fault Accident

When a driver is at fault, car insurance coverage becomes the main way losses are handled. Liability insurance usually applies first. It affects how damage and injury claims move forward and where personal responsibility may begin.

Confusion often arises because different types of coverage apply to different parts of a claim.

- Collision coverage versus liability insurance

Collision coverage may apply to the at-fault driver's own vehicle. Liability insurance applies to damage or injuries suffered by the other driver. - Personal injury protection and medical payments coverage

These coverages may help with certain medical expenses, depending on the policy and circumstances. - Whether there is enough insurance coverage

When costs exceed policy limits, insurance may not cover everything. Remaining losses may fall back on the at-fault driver.

How Coverage Typically Responds

How insurance responds after an at-fault accident depends on the type of loss involved and whether policy limits are reached. The table below shows how coverage typically applies and where personal responsibility may remain.

| Situation | What Insurance Usually Covers | What May Fall on the Driver |

| Property damage only | Vehicle repairs up to actual cash value | Deductibles or uncovered repair costs |

| Injury claims | Medical expenses within policy limits | Driver's medical bills or lost wages |

| Shared fault | Reduced claim payment | Partial financial responsibility |

| Damages exceed limits | Insurance pays up to limits | Personal exposure |

National data from the CDC shows injury claims drive far higher costs than property damage alone, which explains why higher insurance premiums often follow at-fault crashes.

Liability Coverage After an At-Fault Accident

Liability coverage pays claims made against the at-fault driver, up to the policy limits. That coverage applies to damage and injuries suffered by the other driver, not to losses tied to the at-fault driver's own vehicle. The amount the insurance pays depends on the policy and the assigned fault.

Once those limits are reached, insurance stops paying. That gap matters most when serious injuries are involved or when medical costs continue over time. In those situations, expenses can exceed coverage faster than many drivers expect.

Property Damage vs. Bodily Injury Claims

Property damage claims focus on car repairs and vehicle damage. These claims rely on inspections, estimates, and repair timelines. They usually resolve faster, unless damage is disputed or the vehicle is declared a total loss.

Bodily injury claims move more slowly. Medical records, treatment plans, and recovery timelines affect insurers' value assessments. Disputes are more common, especially when symptoms worsen or treatment continues after the initial evaluation.

When Damages Exceed Policy Limits

When insurance coverage runs out, responsibility does not end. Insurance may pay part of the claim, but the remaining losses do not disappear. Medical bills, repair costs, and lost wages above policy limits may still be owed.

This is where coverage gaps become clear. Drivers may face direct financial responsibility even after insurance has paid its maximum amount. These situations often lead to disputes and increased legal exposure.

What Happens After a Car Accident That Is Your Fault

After a crash, the insurance claim process rarely moves all at once. It unfolds in stages, often stretching out when responsibility, injuries, or coverage limits come into question. Even when fault seems clear at the scene, insurers still review evidence before deciding how a claim moves forward.

The process usually follows this path:

- The claim is reported to the insurance agent

- An insurance adjuster investigates how fault is determined

- Vehicle damage and actual cash value are assessed

- Medical treatment continues, and records accumulate

- Claims are negotiated, delayed, or disputed

Delays are more likely when driver responsibility is shared, injuries evolve over time, or policy limits affect the insurer's willingness to pay.

Do You Need an At-Fault Accident Attorney?

At-fault accidents rarely stay simple. Fault can be shared, injuries may evolve over time, and insurance coverage often has limits that are not immediately apparent. As claims move forward, details that once seemed minor begin to affect liability and compensation.

An at-fault accident attorney becomes valuable when responsibility is disputed or injuries require ongoing care. These cases are drawing closer scrutiny from insurers, and coverage limits may fall short of total losses. As claims escalate, managing communication and protecting credibility become very important.

Legal representation helps contain risk at each stage of the process. An attorney can handle interactions with insurers, prevent damaging statements, and challenge attempts to limit or deny claims. That support often matters most before drivers realize how much exposure an at-fault accident can create.

Frequently Asked Questions About At-Fault Car Accidents

After an at-fault crash, questions tend to surface once insurance claims and liability issues begin moving forward. The answers below address common concerns drivers have when they are responsible for a car accident in Florida.

Will my insurance rates go up if I'm at fault?

Insurance rates often increase after an at-fault accident, but the size of the increase depends on your policy, driving history, and the severity of the crash. Some insurers offer accident forgiveness, while others adjust premiums at renewal. Rate changes are usually driven by risk reassessment rather than by a single factor.

Can I be sued if I caused the accident?

Yes. If injuries or property damage exceed available insurance coverage, the other party may file a lawsuit. Lawsuits are more common in crashes involving serious injuries, long-term treatment, or disputed fault. Liability exposure depends on coverage limits and how fault is assigned.

What if the other driver was partially at fault?

Florida follows a comparative fault system, which allocates responsibility based on proportionate fault. If both drivers contributed to the crash, liability may be divided by percentage. Shared fault can reduce how much each party may recover and affect how insurance pays claims.

Why Legal Guidance Matters After an At-Fault Accident

When you are at fault for a car accident, the situation is rarely simple. Fault determinations can shift. Injuries may surface later. Insurance decisions made early often influence outcomes long after the crash itself.

At JDLE Lawyers, we review accident reports for errors, challenge unfair interpretations, and step in when liability or coverage exposure grows. Our team represents clients across Miami, Hialeah, Coral Gables, Aventura, and throughout South Florida.If you were involved in a car accident and questions about fault or insurance are already coming up, timing matters. An initial consultation can clarify your options and help prevent small issues from becoming larger problems. Protect your position and your future.Contact JDLE Lawyers now.